A consumer loan is a type of credit that is given to a borrower to fund specific expenditures. These can include home purchases, debt consolidation, education, and general living expenses.

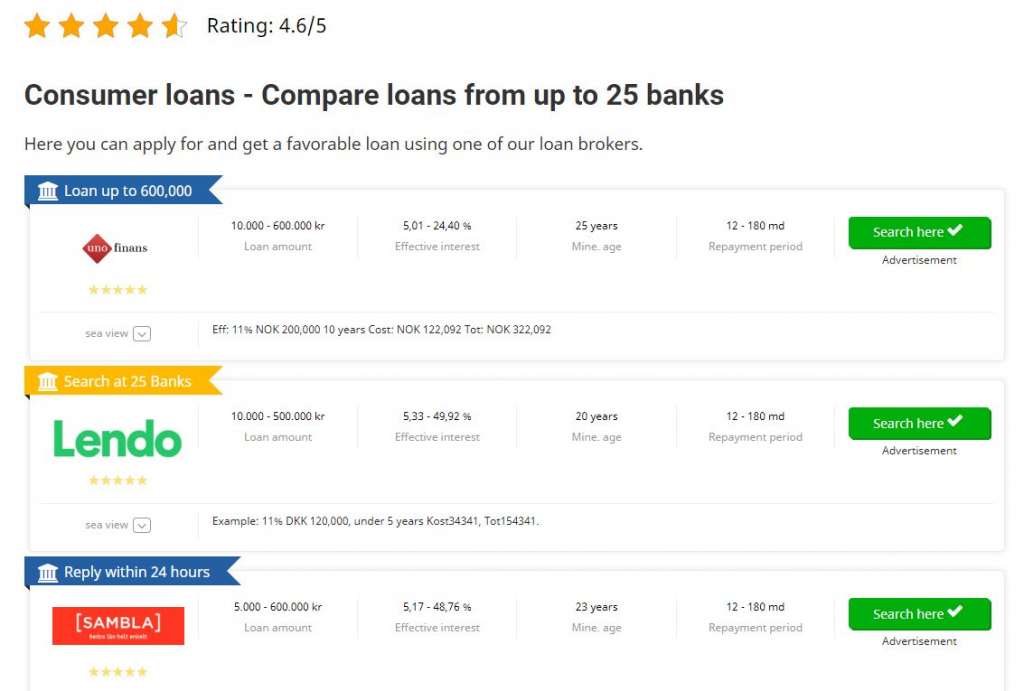

This type of loan can be secured or unsecured. Secured loans require collateral (assets that can be used to cover the loan in the event that the borrower defaults) and usually have a longer repayment term and lower charged interest rate than unsecured loans. You should contact a loan broker to get Forbrukslån – Søk Hos 25 Banker Med Kun 1 Søknad ~ Finanza.

Unsecured

A consumer loan is a type of financing that lets you borrow money to buy a product or use a service. It typically comes with interest and is paid back in installments over time. It is one of the most popular ways for consumers to pay for large purchases and to save on cash outlays.

There are a variety of consumer loans, and each one has its own unique terms and interest rates. Some, like mortgages and car loans, are secured whereas others, such as credit cards, are unsecured.

Secured debts require collateral to protect the lender in case you default on the loan. This can be a home or car, but it can also be an asset such as a bank account or savings account.

Unsecured debts do not require collateral, but lenders still charge a higher rate of interest for these types of loans than secured loans. Examples of unsecured loans include credit cards, personal loans and student loans.

How Does an Unsecured Loan Affect your Credit?

Defaulting on an unsecured debt, such as a credit card or loan, can have negative impacts on your credit. It can hurt your score and report to the credit bureaus, so you should always repay debt on time.

The lender may also report your credit payment history to the credit bureaus, which can hurt your score even more if you default on multiple debts or fail to make payments at all. If you default on a secured debt, such as a mortgage or auto loan, the lender can take your property and sell it to get its money back.

This can be a bad situation for you, but it is not always your choice. If you are unsure about the best way to finance a new purchase or consolidate debt, it is best to talk with a financial expert about your options and decide which is right for you.

You should also consider how the type of consumer loan you choose will affect your credit and whether it is the best option for you. For example, a home equity loan can be more beneficial to you than an unsecured loan, as the proceeds from the sale of your home can be used to help pay off the balance on your loan.

A creditor can use your unused credit to increase your credit limit, or it can offer you a lower-interest rate. However, it is important to understand that if you use your credit more than you can afford to repay, you will pay more in interest over the life of the loan. This can make it difficult to make ends meet if you are paying high interest rates and have a lot of debt.

Types of Consumer Loans You Can Apply For

Consumer loans are a type of financing that makes it possible for people to buy things they otherwise could not afford. These types of purchases can be anything from a new car to a vacation.

These loans are issued by financial institutions and private lenders. Some are unsecured, while others require collateral.

Credit Cards

Credit cards are a popular form of revolving credit that you can use to make purchases and pay for them in installments. They’re available from a variety of financial institutions, including banks and credit unions.

Credit card issuers typically set credit limits based on an individual’s financial situation and history. They also offer rewards programs for consumers, such as airline miles, hotel rooms and gift certificates.

In many cases, credit card holders also get a cash advance, which allows them to withdraw a small amount of money from a bank branch or ATM. This type of credit isn’t ideal for most people, though, because it has high interest rates and fees that can quickly add up to a lot of money.

Before applying for a credit card, you should research its features and benefits to ensure it’s the right fit for your needs. Picking the wrong card can cause you to lose out on valuable opportunities, and may even damage your credit score.

Auto Loans

A car loan is a type of consumer loan that helps you finance the purchase of a new or used vehicle. It consists of a lender lending you the money to buy a car, then allowing you to pay back the loan via monthly payments.

A good credit score and a history of making timely payments are key requirements for auto loans. Some lenders also consider your debt-to-income ratio.

You can get preapproved for a car loan before you go to the dealership by filling out forms with banks, credit unions or online lenders. This can help you find the best interest rate and give you bargaining power with the dealership.

Lenders typically approve an auto loan if your income is adequate and your credit report shows that you have a credit utilization rate of no more than 30 percent of your available credit. However, you should apply for a loan only after you have done all of your research and determined that an auto loan is the best choice for you.

Education Loans

Education loans are a type of financial aid designed to help students pay for their higher education. Like other loans, they require repayment, but unlike most other types of debt, education loans often have a low fixed interest rate that remains the same over the life of the loan.

The federal government offers student loans that can be applied for by completing the Free Application for Federal Student Aid (FAFSA). These loans are available for both undergraduate and graduate students, and they typically offer both subsidized and unsubsidized options.

Another type of student loan is private loans, which are made by individual lenders. These aren’t federally-regulated loans, and interest rates can be lower or higher than those offered by the federal government.

While federal student loans are generally the best option for many college-bound students, private loans are a good alternative when the federal program doesn’t cover all of the cost of attendance or when you need more flexible repayment terms. Using sites like Credible, you can compare private loans in real time and find the right one for your situation.

Refinance Loans

Refinance loans allow borrowers to change the terms of their existing mortgage, auto loan or credit card debt. These changes may include lower interest rates, longer loan repayment periods or a combination of both.

Refinancing can save borrowers money in the long run, but it can also cause your credit score to take a hit. Because of this, you should always prequalify for a refinance loan before applying to see how much you can borrow and what your new monthly payment would be.

Using your equity to fund other financial needs is another common reason people choose to refinance their home. This can be done with a cash-out refinance, which gives you the funds you need to pay off your mortgage, or through a rate and term refinance, which offers a lower interest rate and a new loan term.

Before you refinance your personal loan, check with your lender to determine your outstanding payout balance and learn about prepayment penalties. These penalties can cost you a lot of money and could outweigh the savings you’ll receive by refinancing.